The Truth about Mortgage Qualifying in Ontario

You've done everything right. You have a steady job, you've been saving diligently, and you're ready to buy your first home in Ontario. Then the bank says no — or worse, you get a mortgage approval that's far lower than what you expected. What went wrong?

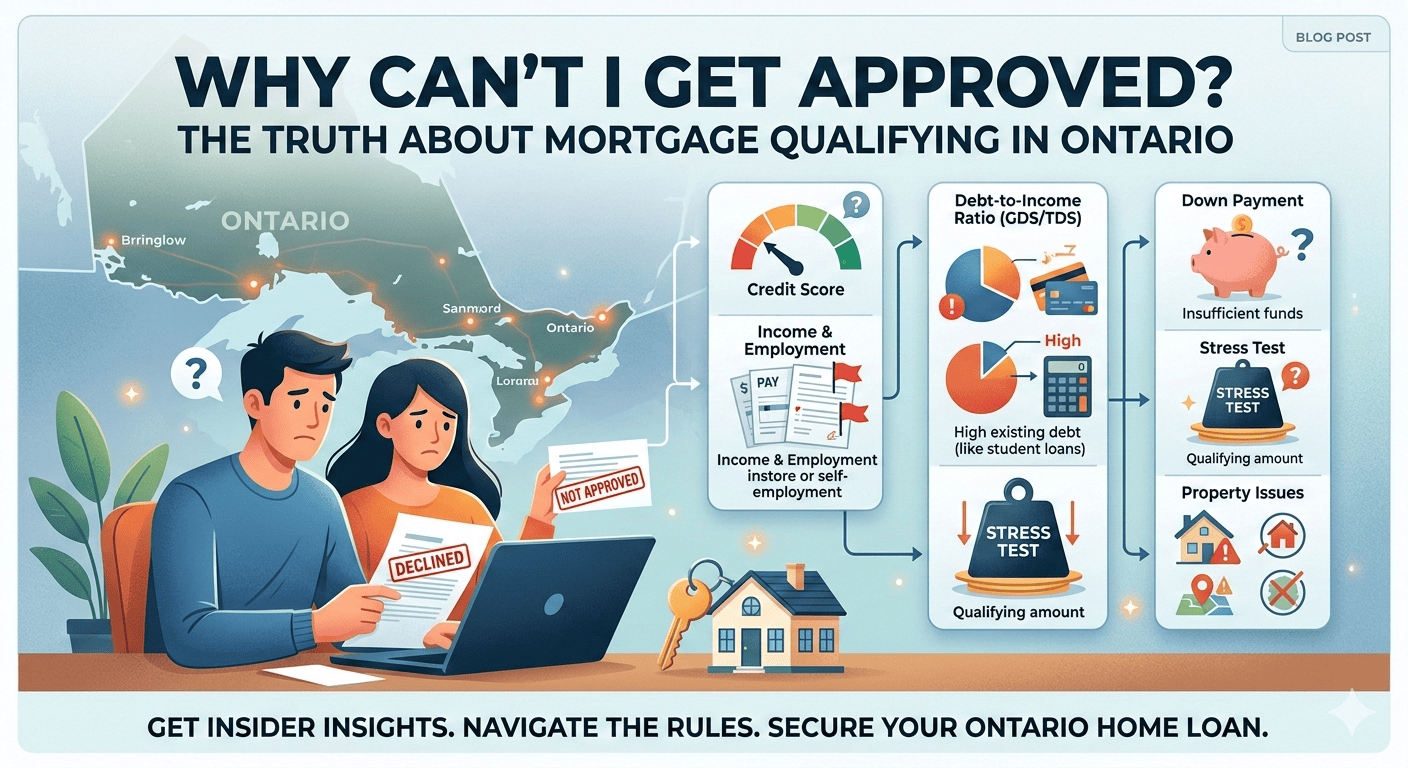

Getting declined for a mortgage is more common than most people realize — and it's almost never because you're "bad with money." The mortgage qualifying system in Canada is complex, counterintuitive, and full of rules that even financially savvy people don't know exist.

This article will walk you through exactly how mortgage qualification works in Ontario, the most common reasons people get declined (even when they shouldn't), and — most importantly — what you can do about it.

1. The Stress Test: Canada's Most Misunderstood Mortgage Rule

If there's one rule that catches Ontario buyers by surprise more than any other, it's the mortgage stress test.

Introduced nationally in 2018, the stress test requires that all mortgage applicants — even those with large down payments — qualify at a rate higher than the rate they'll actually pay. As of 2025, that qualifying rate is the higher of:

• The Bank of Canada's conventional 5-year posted rate (currently 5.25%), or

• Your contracted mortgage rate plus 2%

So if you're getting a 4.89% mortgage rate today, you'll be stress-tested at 6.89%. In practical terms, this means the bank is asking: 'Could this person afford their payments if rates rose by 2%?' If the answer is no, you don't qualify — even if today's payment is perfectly manageable.

📊 Real-World Example You earn $95,000/year. At your actual rate of 4.89%, you might qualify for a $620,000 mortgage. But after the stress test at 6.89%, your maximum qualification drops to roughly $520,000 — a $100,000 difference. That gap can make or break a deal in Ontario's market. |

The stress test applies to virtually every mortgage in Canada, including refinances and switches to a new lender. The only exception is certain uninsured renewals with the same lender — though even that comes with its own complications.

💡 Pro Tip: Many buyers don't realize the stress test also applies when you switch lenders at renewal. That's why talking to a mortgage agent before your renewal is critical — we can help you navigate this and still find you a better rate. |

2. GDS and TDS Ratios: The Math Behind Every Approval

Beyond the stress test, lenders use two debt ratios to determine how much mortgage you can carry. Understanding these ratios is the key to understanding why you may have been declined — or why your approval came back lower than expected.

Gross Debt Service (GDS) Ratio

Your GDS ratio looks at your housing costs as a percentage of your gross monthly income. It includes:

• Your monthly mortgage payment (calculated at the stress test rate)

• Property taxes

• 50% of condo fees (if applicable)

• Heating costs (typically estimated at $150/month)

Most lenders want your GDS ratio to be no higher than 39%. Exceed that, and your application gets flagged — even if you've been comfortably paying rent that's higher than the projected mortgage payment.

Total Debt Service (TDS) Ratio

TDS takes everything in GDS and adds all your other monthly debt obligations — car payments, student loans, credit card minimums, lines of credit, and any other regular debt payments. The limit here is 44%.

Your Finances | Numbers |

Your monthly gross income | $7,500 |

Max GDS (39%) | $2,925 / month |

Max TDS (44%) | $3,300 / month |

Your car payment + student loan | $750 / month |

Remaining room for mortgage + housing | $2,550 / month |

Estimated mortgage this supports | ~$385,000 – $410,000 |

Notice how a $750/month car payment meaningfully reduces your maximum mortgage. This is one of the most common — and most solvable — reasons buyers get approved for less than they expected.

3. The Top 5 Reasons Good Buyers Get Declined in Ontario

In over a decade of working with Ontario buyers, here are the most common reasons financially capable people are declined — and what to do about each one.

65% of declined applicants had a fixable issue — they just needed the right guidance before applying. |

❌ Reason 1: Too Much Debt Relative to Income

Even high-income earners get declined when their total debt load is too high. Car leases, student loans, and credit cards all count against your TDS ratio. One common culprit: a co-signed debt (like a child's car loan) that shows on your credit bureau even if you're not the one making payments.

Fix it: Pay down high-balance debts before applying. Even reducing a credit card from $8,000 to $2,000 can improve your ratio meaningfully. If possible, pay off and close accounts you no longer need.

❌ Reason 2: Self-Employment Income That Doesn't Qualify

If you run a business, your tax returns may show far less income than what you actually deposit into your account — because you've written off business expenses (as you should). But lenders use your line 15000 net income from your Notice of Assessment, not your deposits.

Fix it: Talk to your accountant and a mortgage agent before filing your next two tax returns. There are also alternative mortgage products designed specifically for self-employed Canadians. We'll cover this in a dedicated article in this series.

❌ Reason 3: Credit Score Below the Threshold

Most A-lenders (your major banks and credit unions) want to see a credit score of at least 680, with many preferring 720+. A single missed payment, a maxed-out credit card, or a collections account can drag your score below that threshold quickly.

Fix it: Pull your free credit report from Equifax or TransUnion, dispute any errors, and give yourself 3–6 months to improve your score before applying. We cover the full credit playbook in Article 7 of this series.

❌ Reason 4: Not Enough Time at Your Job

Lenders love stability. If you started a new job recently — even with a higher salary — many lenders want to see at least 90 days of employment before they'll approve you. For anyone on probation, approval can be even more challenging.

Fix it: If you're mid-probation, wait it out before applying. If you switched jobs within the same industry at a similar or higher income level, some lenders will make exceptions with a letter from your employer.

❌ Reason 5: The Down Payment Can't Be Verified

Even if you have the money, lenders need to see a clear 90-day paper trail of where it came from. Cash savings that aren't in a bank account, international transfers without documentation, or money from a family member without a proper gift letter can all create problems.

Fix it: Start documenting your savings now — even if you're a year away from buying. If you're receiving a gift, your mortgage agent will walk you through exactly how to document it properly.

4. Mortgage Agent vs. Going Straight to Your Bank: A Critical Difference

If your bank declined you, it's tempting to assume the answer is simply 'no.' But here's what most buyers don't realize:

Your bank only has access to their own mortgage products and their own qualifying criteria. A licensed Ontario mortgage agent has access to 30+ lenders — including major banks, credit unions, trust companies, and alternative lenders — each with different qualifying rules, rate specials, and appetite for different borrower profiles.

Going to Your Bank | Using a Mortgage Agent |

Number of lenders available | 1 (their own) |

Cost to you | Free |

Works in your interest | No — bank employee |

Can shop multiple options | No |

Knows alternative products | Limited |

Can explain a declined application | Rarely |

Beyond product access, a mortgage agent reviews your full financial picture before you apply — so you know your approval odds before any lender pulls your credit. That matters because every hard credit pull slightly affects your score.

5. What to Do If You Were Recently Declined

A declined mortgage application is not the end of the road. Here's a clear, practical path forward:

1. Get the specific reason in writing. Lenders are required to tell you why they declined you. Request it if they didn't provide it.

2. Don't apply to multiple banks. Each hard credit inquiry lowers your score slightly. Multiple applications in a short window compound the damage.

3. Talk to a mortgage agent immediately. We can review the decline reason, identify the right lender for your profile, and often get an approval the bank couldn't provide.

4. Build a 90-day plan. In most cases, a targeted 3-month plan addressing the specific decline reason is enough to get you from 'no' to 'approved.' This might include paying down a specific debt, adding a co-borrower, or building 60 days of additional employment history.

5. Consider alternative lenders. B-lenders and private lenders exist for a reason. They carry higher rates, but they can bridge the gap while you strengthen your application for a conventional mortgage later.

The Bottom Line

Being declined for a mortgage in Ontario doesn't mean you can't buy a home. In most cases, it means there's a specific, fixable issue standing between you and your approval — and that issue can be addressed with the right guidance.

The mortgage qualifying system in Canada is designed to be conservative. But within that system, there are more options, more lenders, and more pathways than any single bank will ever show you. That's exactly where a licensed mortgage agent earns their value.

Whether you were recently declined, are worried you might be, or just want to know where you stand before you start house hunting, the smartest first step is always a conversation — not an application.

Ready to Find Out Where You Stand? Book a free 15-minute pre-qualification call with me — no credit check required, no obligation. I'll give you an honest picture of where you stand and a clear path forward. |

About the Author

This article was written by a licensed mortgage agent in Ontario, regulated by the Financial Services Regulatory Authority of Ontario (FSRA). With access to over 30 lenders, I help Ontario buyers and homeowners navigate the mortgage process with clarity and confidence.

About This Series

This is Article 1 of a 12-part series on Ontario mortgage topics. Each article addresses a real pain point that homebuyers and homeowners face. Look for new articles published weekly.

Topics in this series include: How much can you afford? · Fixed vs. Variable Rate · 2026 Mortgage Renewals · Down Payment Sources · Self-Employed Mortgages · Credit Scores · Payment Shock · Mortgage Agents vs. Banks · Newcomer Mortgages · Breaking Your Mortgage Early · Is Now a Good Time to Buy?