Going through a separation? Learn how you might be able to keep your home—even if you can’t qualify for a mortgage on your own. Get expert strategies and tips.

Going through a separation? Learn how you might be able to keep your home—even if you can’t qualify for a mortgage on your own. Get expert strategies and tips.

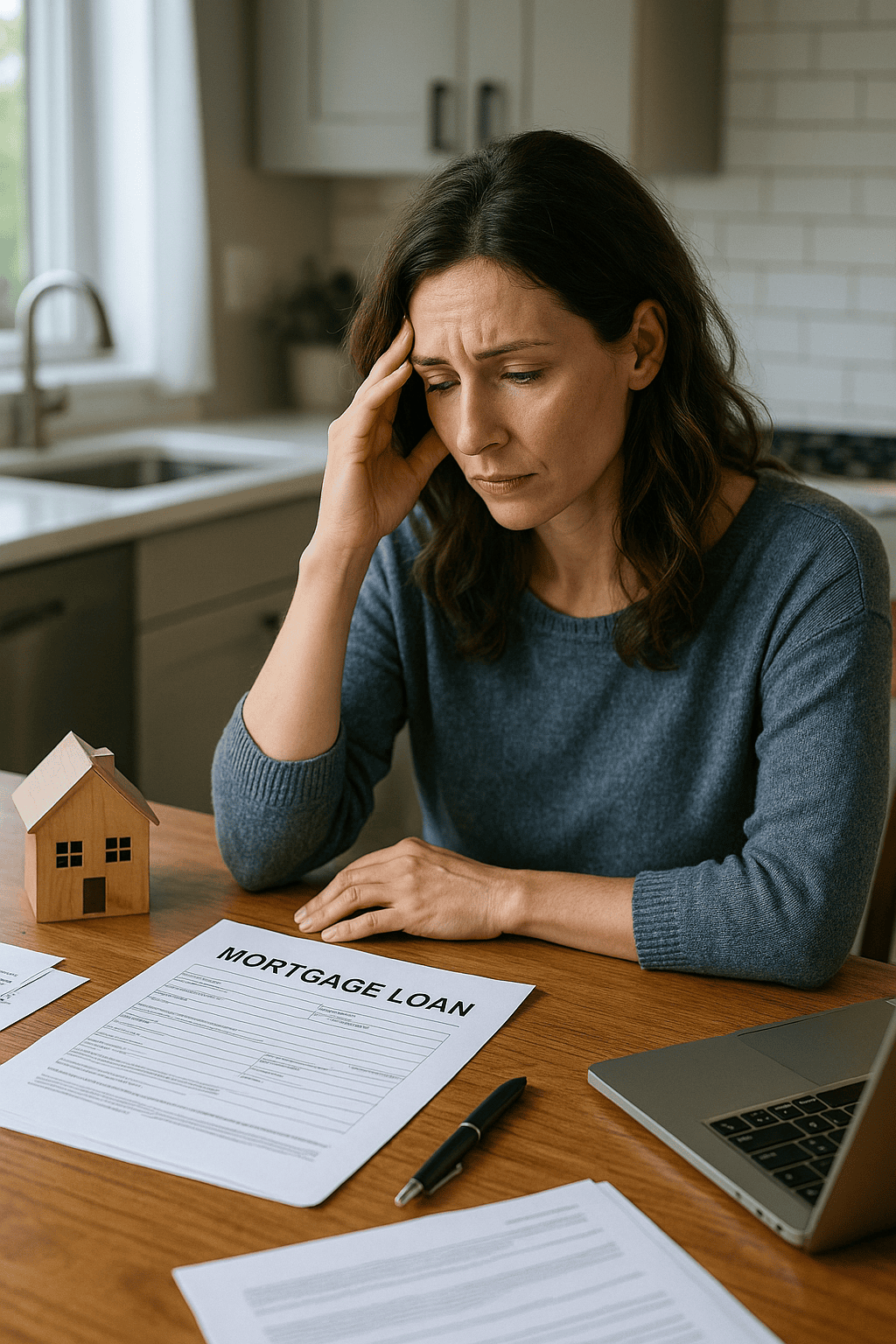

Life After Separation: Can You Still Keep Your Home?

Separation is never easy—emotionally, financially, or logistically. One of the toughest questions people face is, “Can I keep the house?” It’s not just a property; it’s the place where your memories live, your kids play, and your future still feels possible.

But what if you can’t qualify for a mortgage on your own?

Let’s talk about your options. Because yes, you might still be able to stay in your home—even if the bank says “no” at first.

1. Know Your Numbers First

Before making any decisions, it's important to understand your financial picture:

What’s your current mortgage balance?

What’s the home’s market value?

How much equity do you have?

What’s your income now (post-separation)?

A mortgage agent can help you calculate your loan-to-value ratio (LTV) and your debt-to-income ratio (DTI)—two critical numbers lenders look at. You may not qualify alone, but that’s not the end of the road.

2. Introducing the Spousal Buyout Program

This is a little-known program designed exactly for situations like yours.

If you're separating and want to buy out your partner's share of the home, a Spousal Buyout Program allows you to refinance up to 95% of the home’s value—instead of the usual 80% limit on refinances.

✔ You must be legally separated

✔ A formal separation agreement is required

✔ The home must be the primary residence

✔ The property must remain under your name alone

This program essentially treats the transaction like a purchase instead of a refinance, unlocking more equity and flexibility.

3. What If You Don’t Qualify Yet?

Not all hope is lost. There are still options you can explore:

💡 Co-signers or Guarantors

A trusted family member or friend with solid income and credit can step in to help you qualify. They won’t have ownership in the home, but they will be financially responsible for the loan.

💡 Alternative Lenders

Some B-lenders and credit unions are more flexible about income types and credit scores. While the rates may be higher, they could give you time to rebuild your finances before switching to a traditional lender later.

💡 Temporary Rental Strategy

If you can’t keep the home right now, consider renting it out instead of selling. This can help cover the mortgage while you plan a comeback strategy.

4. Work With a Mortgage Agent Who Gets It

Navigating a mortgage post-separation isn’t just about numbers—it’s about understanding the emotional weight behind every decision.

A mortgage agent experienced in family transitions can:

Help you access the Spousal Buyout Program

Connect you with appraisers and legal professionals

Suggest lenders who look beyond just credit scores

Create a step-by-step action plan for long-term stability

5. Don't Rush—But Don’t Wait Too Long Either

Timing matters. The longer things remain undecided, the harder it can become to untangle joint finances. Take time to grieve and think—but once you're ready, start exploring your options. Your future home security depends on it.

Final Thoughts

Yes, separation is difficult. But keeping your home may still be possible—even if you’re facing financial uncertainty. With the right strategy and professional help, you can regain control and build a new foundation—right where your life already began.

Need Help Navigating Your Options?

Let’s talk. I specialize in helping clients through major life transitions—including separation. Contact me for a free, no-pressure consultation and let’s explore your options together.