Credit Score & Mortgage Approval in Ontario (2026 Guide)

Learn how your credit score affects mortgage approval in Ontario. Minimum scores, lender requirements, tips to improve credit, and expert advice from an Ontario mortgage agent.

Introduction: Why Your Credit Score Matters More Than You Think

If you’re planning to buy a home or refinance in Ontario, your credit score can make or break your mortgage approval. Many buyers focus only on interest rates, but lenders look at your credit score first to decide if you qualify, which lender you qualify with, and how much interest you’ll pay.

The good news?

You don’t need a perfect credit score to get approved. You just need the right strategy and the right mortgage agent.

This guide explains everything Ontario home buyers need to know about credit score and mortgage approval in 2025.

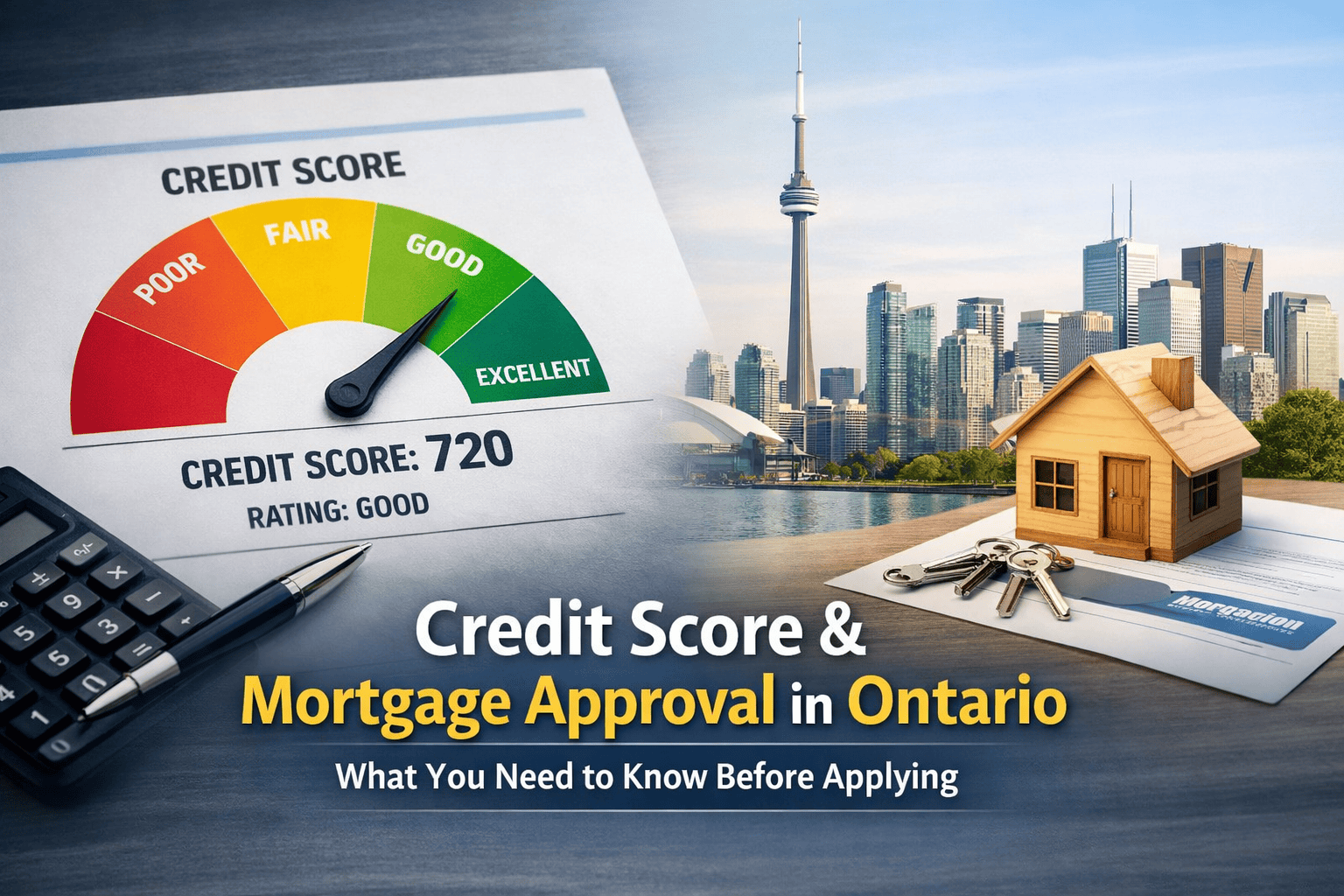

What Is a Credit Score in Canada?

A credit score is a three-digit number that reflects how responsibly you manage debt. In Canada, credit scores typically range from 300 to 900.

Credit Score Ranges Explained

760 – 900 → Excellent

725 – 759 → Very Good

660 – 724 → Good

600 – 659 → Fair

Below 600 → Poor

Lenders in Ontario mainly use data from Equifax Canada and TransUnion Canada.

Minimum Credit Score for Mortgage Approval in Ontario

This is the most common question I get as a mortgage agent.

Credit Score Requirements by Lender Type

A Lenders (Banks & Prime Lenders)

Minimum credit score: 680

Best interest rates

Strict income and debt verification

Stress test applies

B Lenders (Alternative Lenders)

Minimum credit score: 600

Higher interest rates

Flexible income rules

Ideal for self-employed borrowers

Private Lenders

Credit score: Less important

Focus on property equity

Short-term solution

Higher interest and fees

💡 Many Ontario buyers are declined by banks but approved easily through alternative lenders with a solid plan.

How Credit Score Affects Your Mortgage Interest Rate

Your credit score doesn’t just decide approval — it directly impacts your monthly payment.

Example:

Credit score 750+ → Lower interest rate

Credit score 650–679 → Higher interest rate

Credit score below 620 → Limited lender options

Over a 25-year mortgage, even a 0.50% difference can cost or save tens of thousands of dollars.

What Lenders Look at Beyond Credit Score

A strong credit score helps, but lenders in Ontario assess your entire financial profile:

Payment history (most important factor)

Credit utilization ratio

Length of credit history

Types of credit (credit cards, loans, LOC)

Recent credit inquiries

Debt-to-income ratios (GDS/TDS)

Employment stability

Down payment source

Common Credit Mistakes That Hurt Mortgage Approval

Avoid these mistakes at least 6–12 months before applying:

Missing or late payments

Maxing out credit cards

Closing old credit accounts

Applying for multiple loans

Ignoring collection accounts

Cosigning loans without planning

How to Improve Your Credit Score Before Applying for a Mortgage

If your credit score isn’t ideal, don’t worry. Here are proven steps that work for Ontario borrowers:

Practical Credit Improvement Tips

Pay all bills on time (even minimum payments)

Keep credit utilization below 30%

Do not close old credit cards

Limit new credit applications

Pay down high-interest debt first

Check credit reports for errors

Use a secured credit card if needed

⏳ Most borrowers see improvement within 3–6 months with proper guidance.

First-Time Home Buyers: Credit Score Tips in Ontario

If you’re a first-time buyer:

Aim for 680+ credit score

Keep your finances stable before application

Avoid job changes during approval

Save proof of rent payments

Use government incentives wisely

👉 You may also qualify for:

First-Time Home Buyer Incentive

Land Transfer Tax Rebates

RRSP Home Buyers’ Plan

Self-Employed Borrowers & Credit Score Challenges

Self-employed clients often face:

Lower reported income

Business write-offs

Inconsistent cash flow

Good credit can offset income challenges, especially with:

Stated-income programs

B-lender solutions

Strong down payment

FAQs: Credit Score & Mortgage Approval in Ontario

Q: Can I get a mortgage with a 620 credit score?

Yes, with alternative lenders or private options.

Q: Do joint applications use both credit scores?

Yes. Lenders typically consider the lower score.

Q: Does checking my credit score hurt it?

No. Soft checks do not impact your score.

Q: Should I pay off all debt before applying?

Not always. Strategy matters more than zero debt.

Why Work With an Ontario Mortgage Agent?

Unlike banks, a mortgage agent:

Accesses 40+ lenders

Matches you with the right lender for your credit

Builds a credit-improvement roadmap

Saves time, money, and stress

A decline from a bank does not mean a decline overall.

Final Thoughts: Your Credit Score Is Not the End of the Story

Your credit score is important — but it’s not the final decision maker. With proper planning, even borrowers with average or bruised credit can successfully buy or refinance a home in Ontario.

The key is expert advice before you apply, not after a rejection.