The Bank of Canada announced today that it is holding the policy interest rate at 2.25%, keeping the Prime rate steady at 4.45%. For homeowners, buyers, and anyone planning a mortgage move this year, this stability brings both clarity and opportunity.

Below is a clear breakdown of what this decision means, how it affects different mortgage products, and what smart borrowers should consider next.

🔍 Quick Summary of Today’s Announcement

BoC Policy Rate: 2.25% (unchanged)

Prime Rate in Canada: 4.45% (unchanged)

Impact: Payment stability, improved planning confidence, and potentially favourable mortgage decisions

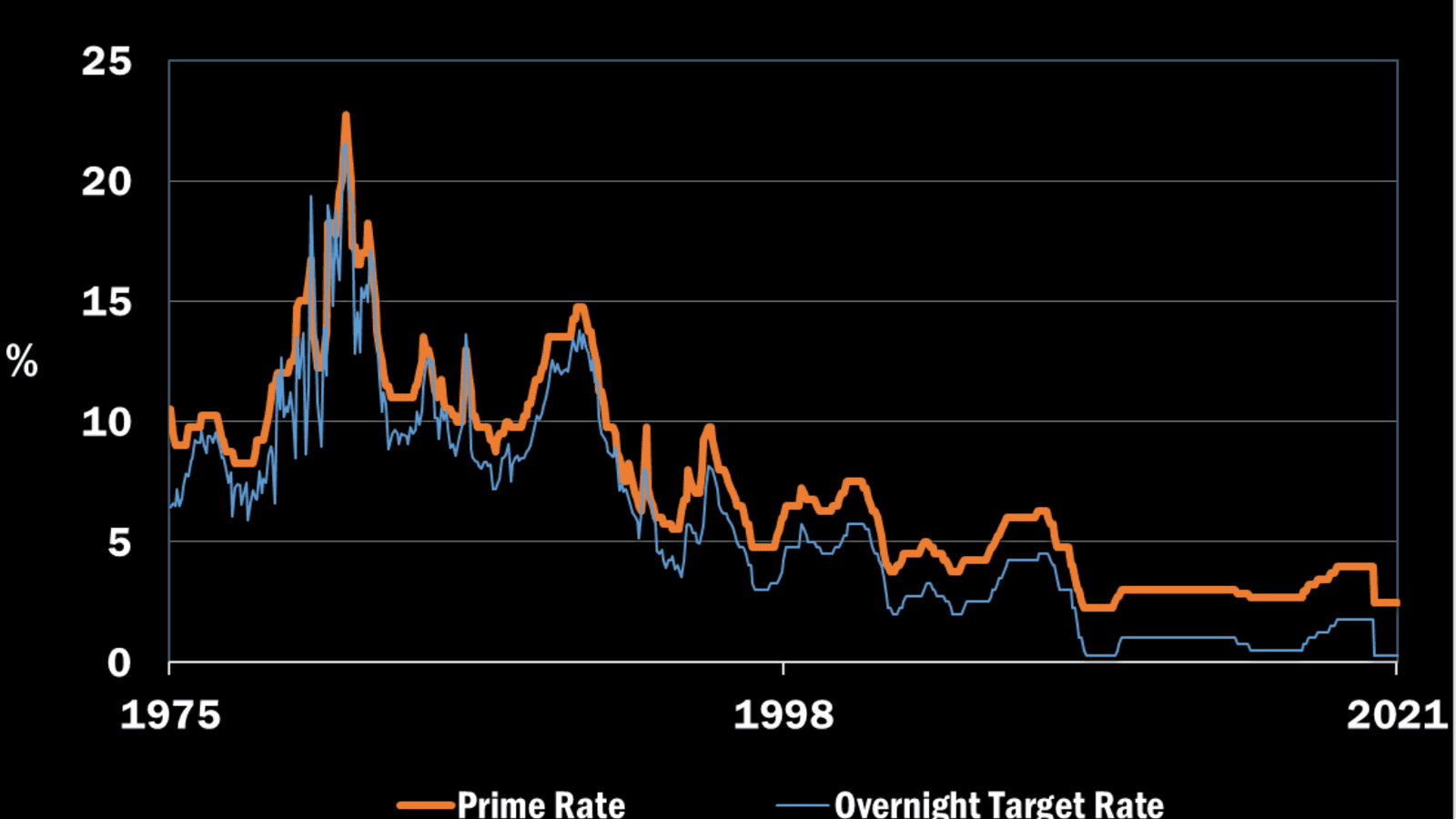

Why Did the Bank of Canada Hold Rates?

The Bank of Canada evaluates inflation trends, employment numbers, economic growth, and global financial conditions.

A rate hold indicates:

Inflation is stabilizing within the bank’s comfort zone

Economic conditions remain steady, with no urgent need for tightening

Borrowers and lenders can expect more predictability in the short term

This creates an environment where households can plan mortgages, renewals, and purchases with greater confidence.

How the 4.45% Prime Rate Affects You

The Prime rate directly influences variable-rate mortgages, HELOCs, and some lines of credit.

If You Already Have a Variable-Rate Mortgage

Your interest rate and monthly payments remain unchanged.

This is a positive signal if you’ve been concerned about fluctuation.

It may be a good time to review amortization and payment strategy.

If You're Considering Switching to Variable

A steady rate environment may offer advantages:

More predictable costs

Potential savings if rates decrease later

Flexibility to lock in a fixed rate at the right time

What This Means for Fixed-Rate Mortgages

Fixed mortgage rates are more closely tied to bond yields than the Bank of Canada’s rate itself.

A rate hold often:

Helps stabilize bond yields, reducing volatility

Creates opportunities to secure competitive fixed rates

Encourages long-term planning for homebuyers and refinancers

If you’ve been waiting for the right moment to renew or refinance, now is a strategic time to reassess your options.

Opportunities for Homeowners and Buyers Right Now

1️⃣ Renewing in the Next 6–12 Months

You may benefit from:

Locking in a competitive fixed rate

Exploring blended or extended terms

Reducing payment shock through early planning

2️⃣ Refinancing to Improve Cash Flow

With stable rates, refinancing can help:

Consolidate high-interest debt

Lower monthly payments

Access equity for renovation or investments

3️⃣ First-Time Homebuyers

This rate hold provides:

More predictable qualification guidelines

Stable stress test expectations

A clearer picture of long-term affordability

Should You Lock In or Stay Variable?

You can edit text on your website by double clicking on a text box on your website. Alternatively, when you select a text box a settings menu will appear. your website by double clicking on a text box on your website. Alternatively, when you select a text box

My Take as a Mortgage Agent

Today’s announcement reflects a stabilizing market—good news for buyers and homeowners.

Stable rates create a window to restructure debt, plan renewals, or enter the market with more confidence.

Every mortgage strategy is unique, especially in Ontario’s fast-moving housing landscape. A personalized review can help you take advantage of today’s steady financial climate.

📞 Want to Understand What This Means for Your Mortgage?

I’m here to review your current mortgage, compare options, and help you make the most strategic decision based on your goals.